Advanced Theory Overview

This page documents the full pipeline and implementation that OIPD uses.

1. End-to-end pipeline

This represents a non-exhaustive, step-by-step pipeline to fit a volatility surface, and subsequently convert it to probability distribution. We’ve documentated the major steps below, as well as explaining OIPD’s implementation.

2. OIPD vs open-source and commercial volatility fitting libraries

OIPD is an end-to-end opinionated volatility surface fitting pipeline, which handles the data plumbing and cleaning, smile/surface fitting, and probability conversion all in one interface.

Other open-source packages, such as QuantLib, provides very strong components for individual stages of the workflow (for example, IV solvers in step 5 and smile/surface fitters in step 6), but it does not natively wire those stages into a single end-to-end pipeline.

OIPD is (or at least aims to be) conceptually closer to commercial libraries like Vola Dynamics than to low-level libraries like QuantLib: it offers an integrated, configurable pipeline for fitting and probability extraction.

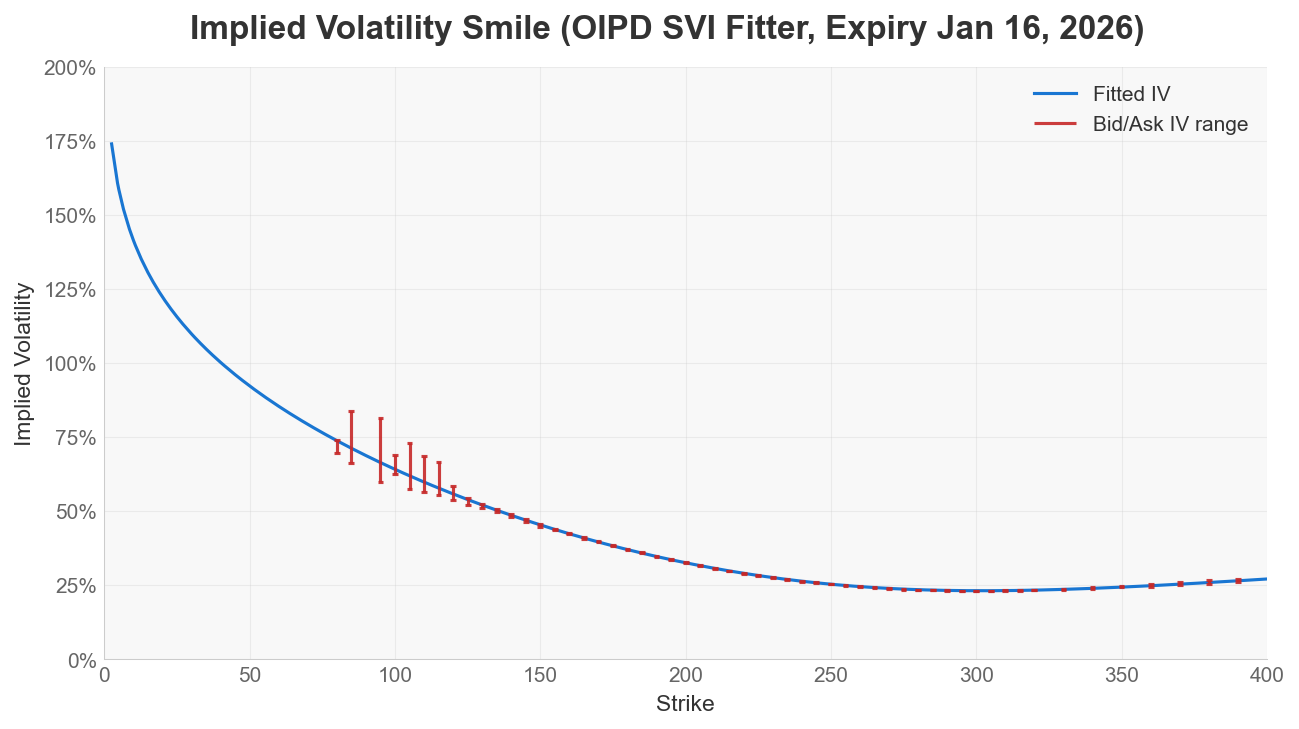

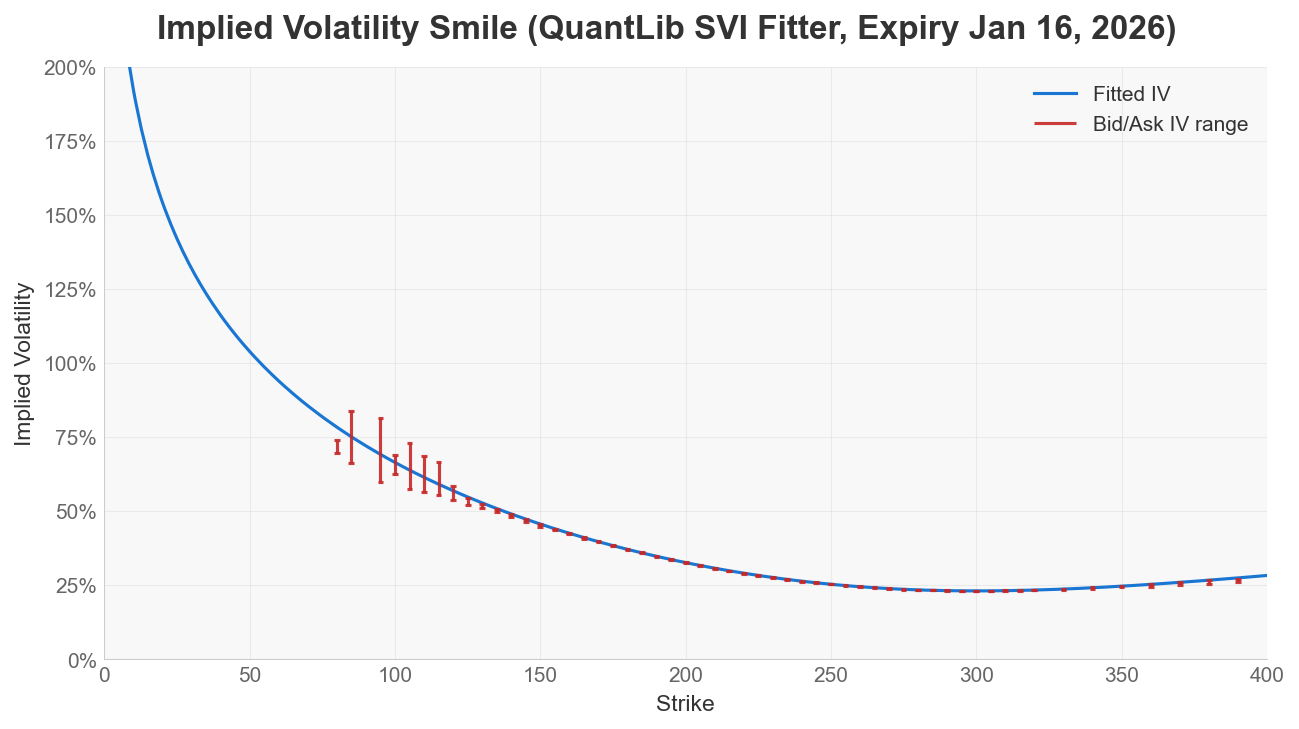

3. Validating OIPD’s SVI fitter

To benchmark OIPD’s SVI fitter, we compare it against a trusted reference: QuantLib’s SVI fitter (SviInterpolatedSmileSection). We keep OIPD’s preprocessing and data-cleaning pipeline fixed, and only swap the SVI calibration step.

The fitted smiles below are shown side by side using the same AAPL dataset and expiry.

OIPD SVI fitter |  QuantLib SVI fitter (OIPD preprocessing + QuantLib calibration) |

To compare a few metrics:

- full pipeline run time

- vega-weighted RMSE

- butterfly arbitrage checks, using 2 checks to detect arbitrage: (1) min(g(k)) and (2) negative density

We find that QuantLib’s SVI fitter is significant faster as it is written in C++, while OIPD ensures no-arbitrage.

| Metric | OIPD SVI fitter | QuantLib SVI fitter |

|---|---|---|

| Full pipeline runtime (mean seconds, 10 runs) | 1.1089 | 0.3647 |

| SVI calibration runtime (mean seconds, 10 runs) | 0.6970 | 0.000374 |

| Vega-weighted RMSE (IV) | 0.01057 | 0.00447 |

| min(g(k)) butterfly check | +0.0820 | -0.0383 |

| Share of grid with g(k) < 0 | 0.00% | 42.26% |

| Negative RND grid points (native 200-point RND grid) | 0 | 14 |

For arbitrage checks, higher min(g(k)) is better, and any negative value is a warning for butterfly arbitrage. Likewise, lower values are better for both Share of grid with g(k) < 0 and Negative RND grid points; 0 is the clean no-violation outcome on the tested grid.